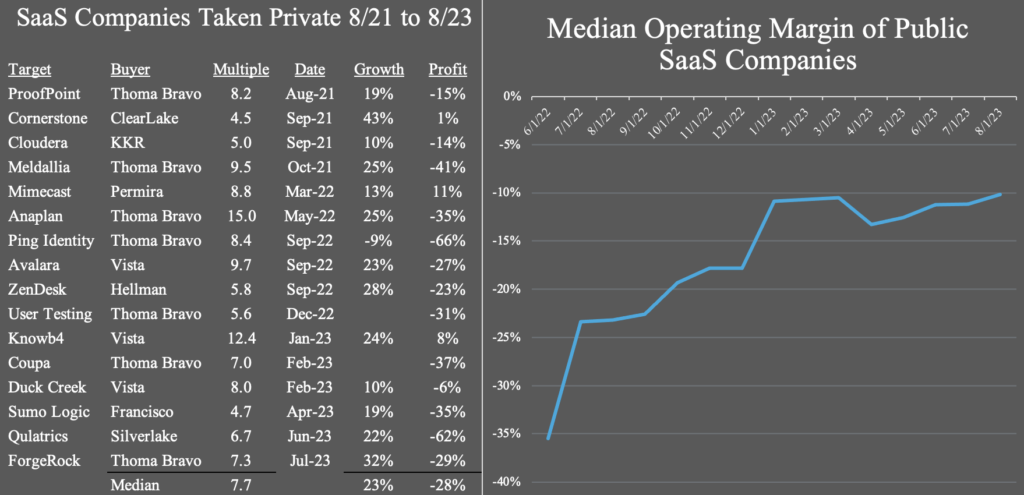

Sixteen public SaaS companies have been taken private in the last two years. Sixteen!

What’s going on, and what can we learn from the PE firms that led these transactions? Let’s look at the data.

First off, while the PE firms were undoubtedly looking for value, that did not necessarily mean “cheap.” They paid, on average, 7.7 times ARR when acquiring a company, which was only about 1.7 times below the average ARR of public SaaS companies at the time of the acquisition. Private buyers are looking for undervalued and underperforming SaaS companies, not just cheap ones.

My colleague David Spitz characterized it like this: “The PE buyer is one of the best things that ever happened to public SaaS. It’s like the ‘cleaner fish’ — ensuring that companies who aren’t being smart about attacking the growth/profit paradigm are subject to being taken out of the game.”

Exactly.

Referring back to my post a few weeks ago, “Pick a Lane,” all but one of the companies acquired by the PE firms were in the Dead Zone or Grey Zone – meaning they were underperforming on the Rule-of-40, specifically, the profit side of that equation.

The growth profile of the companies taken private was about the same as the universe of public SaaS companies at 22%; profits, however, were a different story. As a group, the companies targeted by PE firms were very unprofitable. Half of the companies had operating losses above 30%, with several running into the 60% loss range. This was substantially worse than other public SaaS companies, which averaged losses of 20% over the same period and are now only losing 10%. Thoma Bravo, the most active buyer, acquired seven companies with an average operating loss of 36%.

The point I made in the Pick a Lane post was that management teams running companies with a low Rule of 40 must intentionally pursue growth or profit and stop trying to do both, at least initially. I lay out some objective measures to determine if growth is a viable strategy, and if not, driving profits must be the imperative. If you don’t do one or the other, someone will do it for you, and that’s what happened to these companies.

The SaaS businesses that were not gobbled up have received the message. The chart shows public SaaS companies’ substantial operating margin improvement over the last fourteen months.

I believe the go-private wave is largely behind us because the low-hanging fruit is picked, debt is more expensive, and more companies have improved profits. David Spitz disagrees, “…when you see public SaaS companies drop ~40% overnight because they missed expectations — you can be sure the PEs are licking their chops!”

The takeaway is that all SaaS companies, even large public ones, must either grow quickly or make money. The relentlessly efficient capital markets will solve that equation if the current owners and management team cannot.